How Credit Unions Can Use AI in the Contact Centre Without Losing the Member Relationship

The member relationship isn't being threatened by AI. It's being eroded by hold times, stretched agents, and unresolved calls. Here's where AI belongs in the contact centre and where it doesn't based on our experience at The GCC.

Nelson Lee

Software engineer at Shopify who has built AI systems, workflows, and automations for millions of merchants. Previously an 8VC Fellow in San Francisco. Computer Engineering from the University of Toronto with a minor in Artificial Intelligence.

There’s a tension at the heart of every credit union’s AI conversation.

Credit unions don’t compete with the big banks on rate alone. They compete on relationship. The member experience, knowing someone’s name, understanding their situation, picking up the phone and reaching a person who can actually help, is the product. So when AI enters the contact centre conversation, the instinct is defensiveness. And that instinct is understandable.

But here’s the thing. Today, the member relationship isn’t being threatened by AI. In most credit unions I work with in North America, it’s already being eroded by hold times, by agents stretched across too many channels, by calls that never get fully resolved because the agent couldn’t find the right answer fast enough. The status quo is the problem. AI is one way to fix it.

The question isn’t whether to use AI in the contact centre. It’s which parts of the contact centre should AI touch, and which parts should stay human.

Start With the Data You Already Have

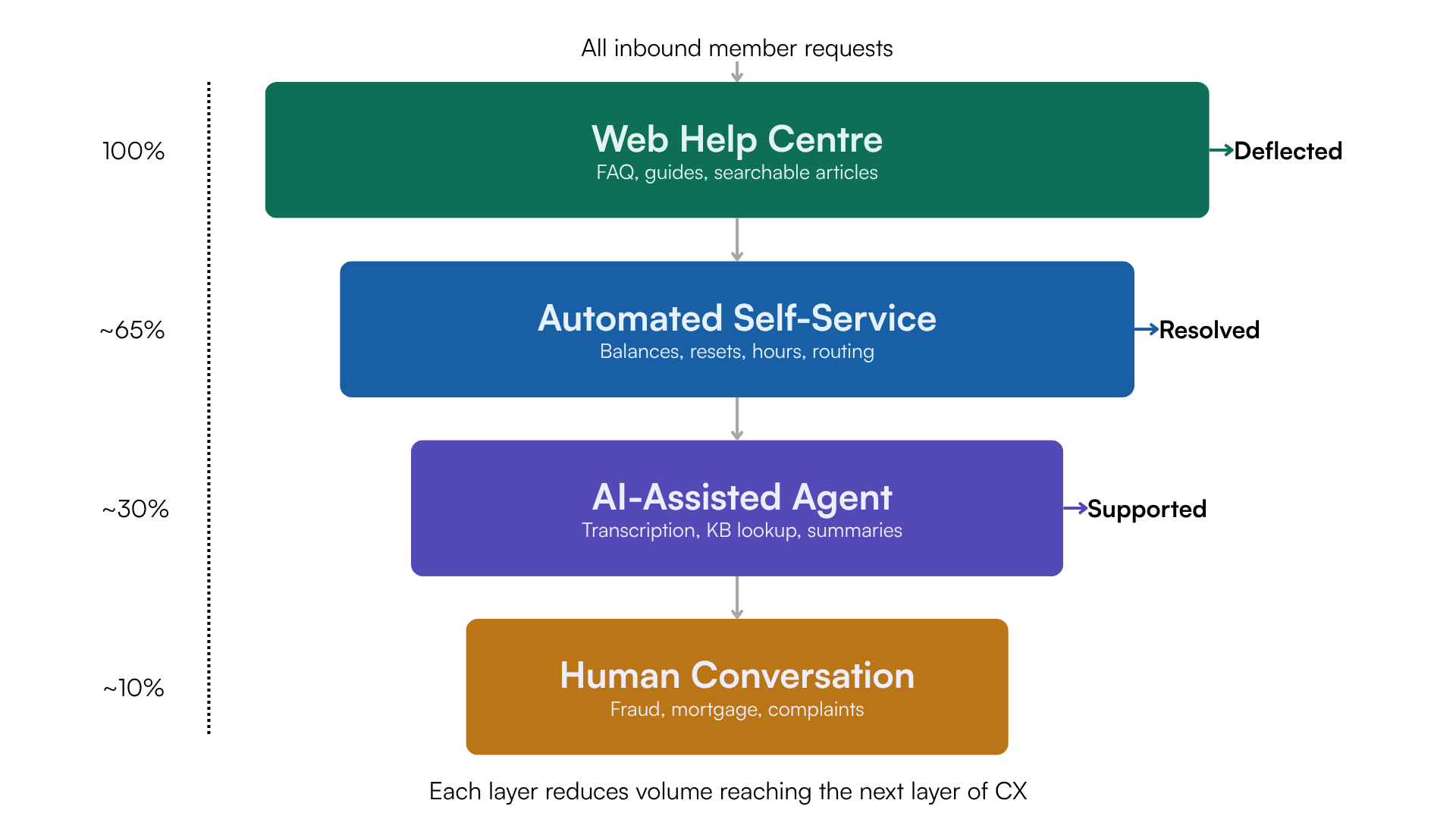

Most credit unions are sitting on more contact centre data than they realize. Disposition reports, call recordings, email volumes. The shape of your member problem is already in there. Before you evaluate a single AI tool, pull that data and categorize it honestly.

What you’ll typically find is a distribution that looks something like this: a third of your volume is routine self-service requests like account balances, password resets, and general product information. Another third is transfers and routing, calls that land in the wrong place and need to get somewhere else. A meaningful chunk is email, often handled manually and inconsistently. And then there’s the catch-all “Other” category, which is usually larger than anyone is comfortable admitting, because it represents everything nobody got around to categorizing properly.

That breakdown tells you exactly where AI creates value, and where it doesn’t.

Where AI Belongs

Routine self-service is the easiest win. Account balances, password resets, hours and location information, basic product questions. These don’t require a human being. They require an accurate, available, fast answer. An AI-powered self-service system handles these 24 hours a day, including nights and weekends when most credit union contact centres are dark. Florida Credit Union reports resolving over 90% of phone conversations without escalating to a human. Citadel Credit Union reduced overflow call costs by 63% and saw member NPS increase after implementing AI in this layer.

But before AI even touches a phone call, the most effective credit unions invest in a well-maintained, searchable help centre on the web. This is the layer most organizations underestimate. A member who can find a clear answer to “how do I set up direct deposit” at 10 PM on a Tuesday never becomes a call at all. AI makes this easier to build and maintain. It can generate draft articles from your most common call topics, keep content current, and surface gaps where members are searching for answers that don’t exist yet. The help centre isn’t a replacement for phone-based self-service. It’s the reason your phone volume drops before automation ever picks up.

The second area is agent support. This is often underestimated. Rather than replacing agents, AI sits beside them in real time, transcribing the call, surfacing relevant knowledge base answers automatically, suggesting next-best actions, and generating after-call summaries. The agent doesn’t have to hunt for answers or spend ten minutes on notes after the call. They can focus on the member. This is where the relationship benefit becomes concrete. When your agents aren’t scrambling for information because AI can supplement information they don’t have, they’re present.

The third area is categorization and analytics. The dreaded “Other” category isn’t just a reporting problem, it’s a signal problem. AI can scan call recordings and email subject lines to identify patterns, build new disposition categories over time, and surface the questions members keep asking that your team hasn’t built a formal answer for yet. That’s intelligence that makes your whole operation smarter, not just faster.

Where Humans Stay In the Loop

Fraud disputes. Mortgage conversations. Anything involving a member who is upset, confused, or in a difficult financial situation. These are not AI interactions. The handoff needs to be seamless, full context carried to the agent so the member never has to repeat themselves, but the human needs to be in the room.

The principle is straightforward: AI handles the predictable, the repetitive, and the information-retrievable. Humans handle the judgment, the emotion, and the compliance risk. A good AI implementation makes your agents more available for the conversations that actually require them, not less.

On Vendor Evaluation

If you’re already using a contact centre platform, start there before looking at new vendors. Many mid-sized credit unions are sitting on AI capabilities they’ve already licensed but never activated. Voice routing, sentiment analysis, real-time agent assistance. These features are often available within existing contracts. A conversation with your account representative about what you have and what it takes to turn it on is almost always worth having before you start evaluating new platforms entirely.

When you do evaluate new vendors, ask specifically about: data training rights (does their model train on your call data?), email channel capabilities (AI marketing is heavily weighted toward voice, and email is often an afterthought), and comparable customer references from institutions of similar size. These allow their AI tools to be more powerful when servicing your clients.

The member relationship is not at risk from AI. It’s at risk from a contact centre that can’t keep up. The credit unions getting this right in North America are the ones using AI to give their best people back the time and attention to do what they do better than any big bank.

If your credit union is exploring AI in the contact centre, we work with institutions across North America on exactly this. Book a free 30-minute call to talk through where to start with The General Consulting Company.

About The General Consulting Company

The General Consulting Company helps business owners and C-suite executives understand and implement AI. We offer practical training, policy frameworks, and custom tooling so your organization can move on AI with confidence.

Not sure where to start? Book a free consultation with The General Consulting Company and we'll walk through what makes sense for your business.

BOOK A CALL